How to Improve Your Credit Score in 6 Months

Simple, proven strategies to boost your score step by step — no complicated jargon.

Why your credit score matters

- Better loan approvals: Higher scores = better chances of approval for loans, mortgages, or cards.

- Lower interest rates: A strong score can save you thousands over time.

- More opportunities: Landlords, employers, and even insurers sometimes check your score.

6-month credit score improvement plan

- Month 1: Check your credit report Get a free copy from major bureaus and dispute any errors. Incorrect entries drag your score down.

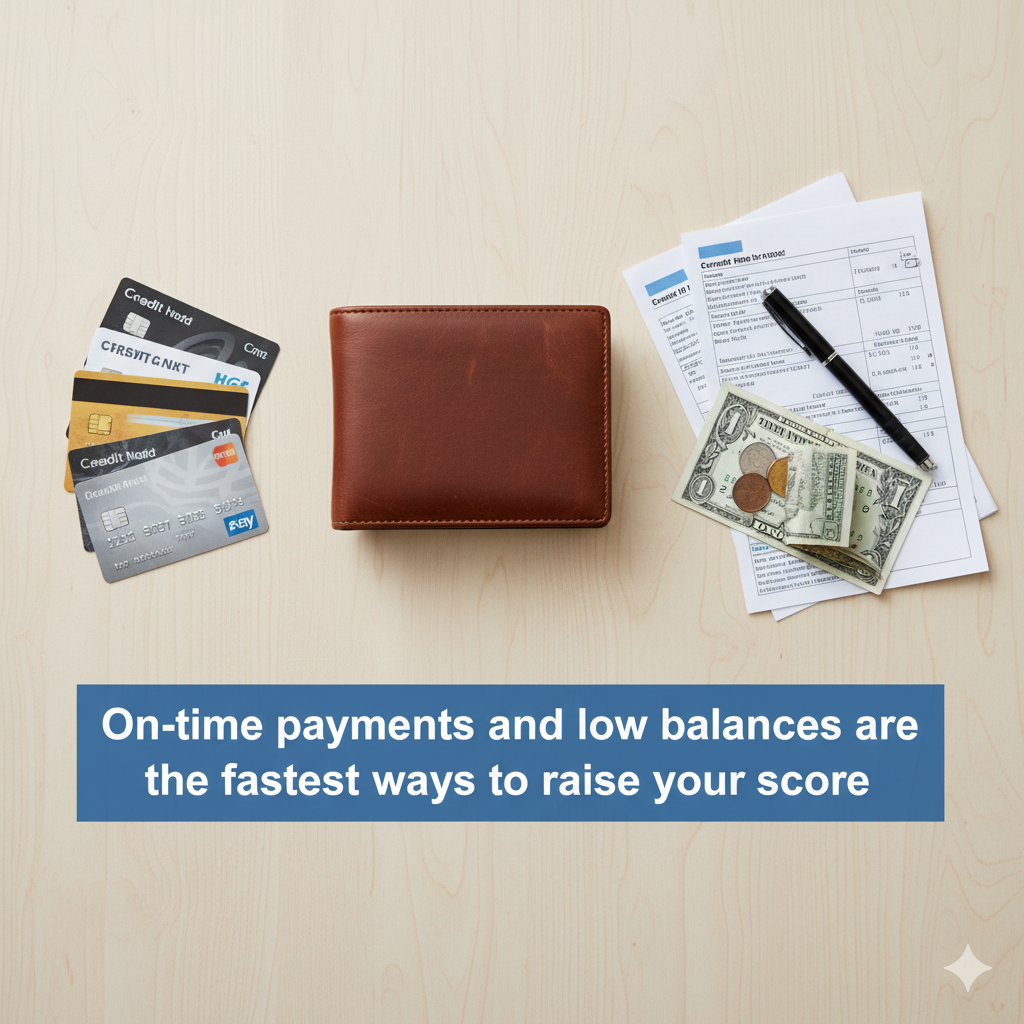

- Month 2: Pay bills on time — every time Set reminders or autopay. Payment history makes up ~35% of your score.

- Month 3: Lower your credit utilization Keep balances below 30% of your credit limit (10% is even better).

- Month 4: Avoid new hard inquiries Don’t apply for multiple new credit cards unless necessary — each hard check lowers your score slightly.

- Month 5: Diversify gently If safe, add a mix (like a small secured card or credit-builder loan). Lenders like variety in credit history.

- Month 6: Keep accounts open & old Don’t close older cards — longer credit history improves your score.

Extra tips for faster progress

- Pay twice a month: Keeps utilization lower when reported to bureaus.

- Use reminder apps: Never miss a payment deadline.

- Ask for a limit increase: More available credit = lower utilization (if you don’t overspend).

- Become an authorized user: A trusted family member’s card with good history can boost your score.

FAQs

How many points can I realistically gain in 6 months?

Many people see a 50–100 point increase with consistent effort, especially if they had negative marks to fix.

Will paying off debt instantly raise my score?

Yes — especially credit card balances. Lowering utilization is one of the quickest ways to see results.

Should I close unused credit cards?

Usually no. Older accounts improve your credit age. Keep them open (as long as they don’t charge high fees).